Against Inflation Hawks

Against Inflation Hawks

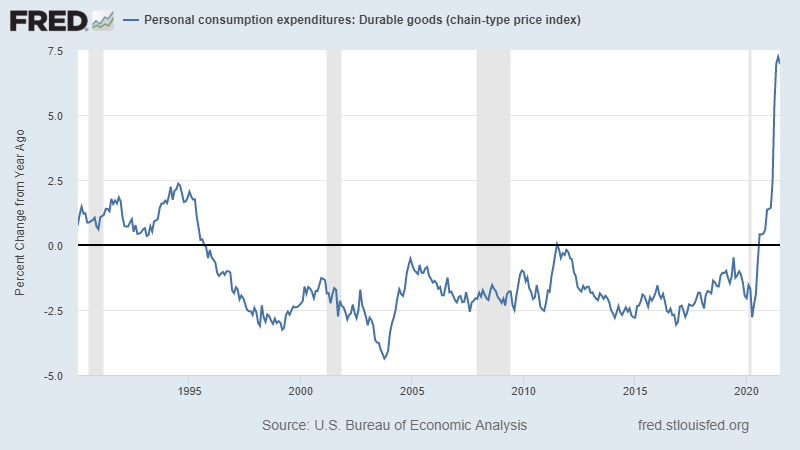

A bit of musing on a cool chart that got my attention.

Hello, friends,

The new inflation numbers are out and the result is that inflation, or consumer price increases, slowed in August after rapidly increasing across 2020 and all of 2021. The Consumer Price Index (CPI) on durable goods edged up 0.1 %, the smallest gain since February, reports Reuters.

The reason this is interesting is mainstream macro economists mostly understood that this was likely the case. Inflation will be transitory and it’s due to legitimate supply chain disruptions and not government spending, or printing money. Supply chains, increasing global, though concentrated across East Asia, most notably China, were shutdown. There was less supply chasing less demand. There are lots of talk about how America and the West should “reshore” production and to make their supply chains more resilient. Obviously more reselient supply chains are necessary because in a warming world, and in a globalized world of hyperfast travel, all but begging for more viral outbreaks, crises are absolutely all but guaranteed over the next few years and decades. However, this graph and complimentary analysis by one of my favorite macro thinkers, Claudia Sahm, shows that globalized supply chains have actually kept inflation in check over the last twenty years, including after China joined the World Trade Organization (WTO) in 2000.

(My source: Stay-at-Home Macro Newsletter; primary source: Fred.stlouisfed.org.)

The horizontal access goes from 1990-2021. The vertical axis is percent change in the chain-type price index of durable goods (goods that are nonperishable such as electronics, vehicles, lumber, etc.) A point above the solid line is an increase over the previous year. A point below would signify a decrease.

Inflation hawks, or those economists or politicians hyperfocused on getting inflation down, caused lots of harm in the 1980s. Hyperfocusing on reducing inflation by raising interest rates costs jobs in the 1980s. And wages are still impacted. The so-called Volcker shock, named after the chairman of the Federal Reserve from 1979-1987, hurt workers. “In fact, American workers did not recover from the Volcker shock. The median income of a full-time male worker in 1978, adjusted for inflation, was $54,392. That number was not matched or exceeded at any point in the next four decades. As of 2017, the most recent available data, the median income of a full-time male worker was $52,146,” writes Binyamin Applebaum (2019, 15%). To put it more bluntly: Paul Volcker caused two recessions, a Latin American debt crisis, and more people died than would have without this focus on inflation (Matthews 2019).

But inflation does hurt consumers:

“Inflation is a loss of purchasing power. If annual inflation is 2 percent, a person with enough money to buy 100 hamburgers on New Year’s Day would be able to afford only 98 hamburgers by Christmas. Consumers do not like the idea that the money in their pocket is losing value. Lenders also dislike inflation: it means the money they get back will be less valuable than the money they loaned. And economists dislike inflation because it reduces the informational value of market prices” (Applebaum 10%. )

But so-called Monetarists who believe that “inflation is always and everywhere a monetary phenomenon” believe in that mantra like a Sunday school preacher believes in whatever it is they believe: on faith or based on doctrine more so than any evidence.

~

Causes matter. The above graph suggests the major cause of the current inflation we are seeing: a shutdown of the global economy due to the global covid-19 pandemic that caused staffing shortages around the world, production bottlenecks, and decreased demand. A July 2021 Federal Reserve report concluded that inflation will be “lasting but likely still temporary.”

All of this is to say that there are lots of problems with our current global political economy, nothing more serious than how environmentally destructive it all is. And distributional questions, both within and between countries are a major problem. Another one is the problem of virtual monopolies with market power. And, lastly, the mechanism of “just in time” supply chains which are constituted of little to no inventory is not going to cut in when multiple, overlapping climate crises occur. For example, in 2011 Thailand had a strong monsoon season that caused record breaking floods. Per a BRS report, close to 15,000 global companies were impacted, and there was a global shortage of hard drive disks through 2012.

The bottomline is that inflation matters but there is no evidence that it should matter more than other issues or human needs: such as high employment, tackling covid-19 through mass vaccination, the quickest path out of this pandemic, and other government priorities such as infrastrucutre bills, paid child credits, and health care provision. Actually understanding the cause of this bout of inflation matters; it is certainly preferable to relying on politicized archaic doctrines that never had strong evidence to begin with.

It’s important to not throw the baby out (global supply chains) with the bathwater (hmm…um…. let’s see: the “organized irreponsibility,” as Adam Tooze puts it in his latest book on the political economy that constituted, in part, how the trajectory and reality of covid shutdowns) when we reform the current neoliberal political economy. There are always trade offs; and there are always unforeseen consequences for any move--major or minor--that one state or multiple states make. We need to build a more resillient global political economy. But global supply chains have kept many different consumer good prices lower than a “beggar thy neighbor” zero-sum nationalistic vs nationalistic neomercantilism alternative model might achieve.

I highly suggest reading the entire newsletter from Claudia Sahm that inspired this newsletter from me HERE.

Take care,

Patrick M. Foran